Commercial Battery Energy Storage As a Service Market Trends, Opportunities and Future Growth

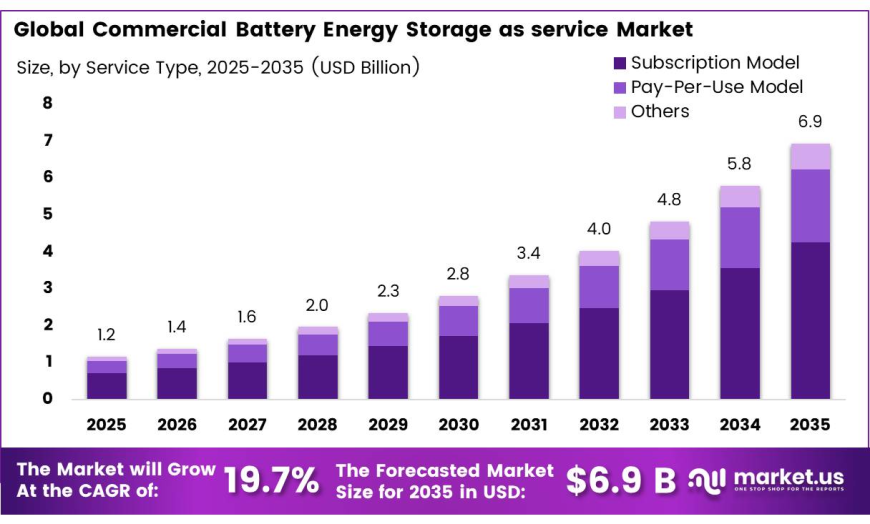

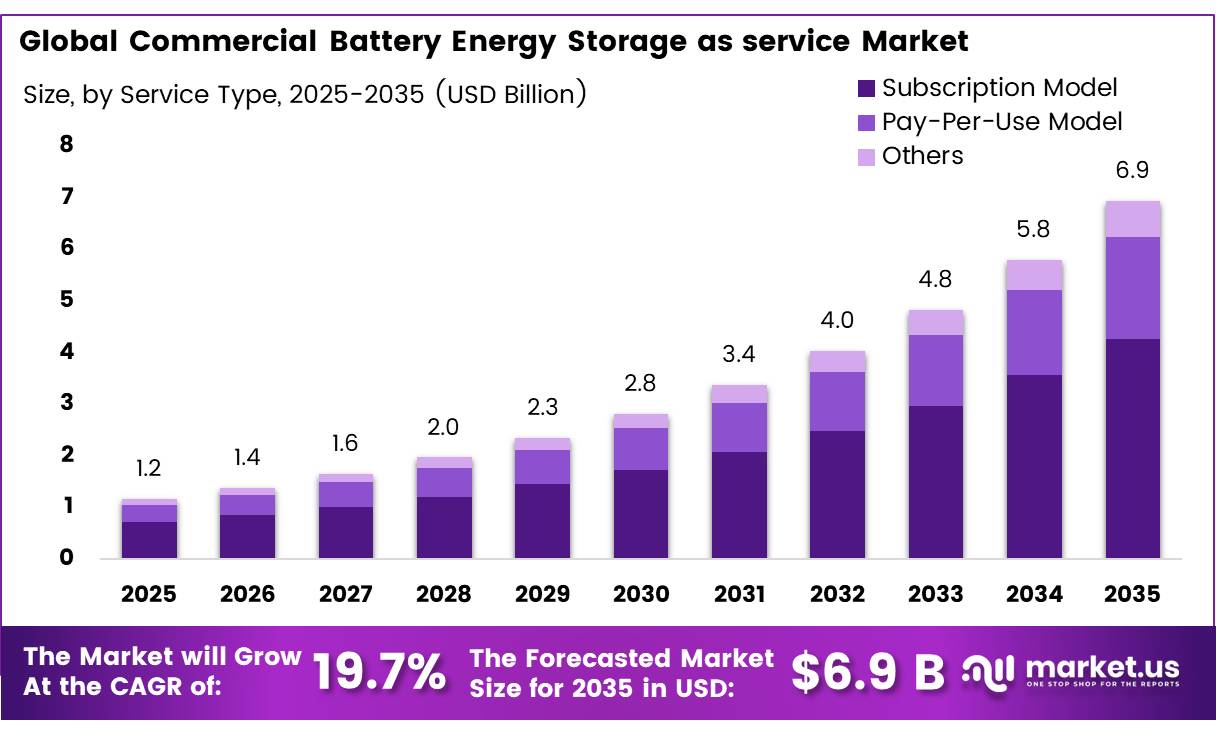

Commercial Battery Energy Storage As a Service Market accounted for USD 1.2 billion in 2025 and is anticipated to reach USD 6.9 billion by 2035, progressing at a CAGR of 19.7%. North America maintained market leadership in 2025, representing 37.0% of the market with revenue of USD 0.4 billion. Rising electricity demand, increasing renewable integration, subscription-based battery storage adoption, and the need for enhanced energy reliability are contributing to continued market expansion.

sonicbolt20

sonicbolt20

Overview

Commercial Battery Energy Storage As a Service Market accounted for USD 1.2 billion in 2025 and is anticipated to reach USD 6.9 billion by 2035, progressing at a CAGR of 19.7%. North America maintained market leadership in 2025, representing 37.0% of the market with revenue of USD 0.4 billion. Rising electricity demand, increasing renewable integration, subscription-based battery storage adoption, and the need for enhanced energy reliability are contributing to continued market expansion.

Key Takeaways

- The Commercial Battery Energy Storage As a Service Market was valued at USD 1.2 billion in 2025.

- The market is expected to reach USD 6.9 billion by 2035, growing at a CAGR of 19.7% between 2025 and 2035.

- By Service Type, the Subscription Model dominated the market with a 61.4% share.

- By Deployment Mode, Behind-the-Meter (BTM) accounted for 65.0% of the market.

- By Enterprise Size, Large Enterprises held a leading 68.5% market share.

- By Industry Vertical, Data Centers captured 35.6% of the market.

- In 2025, North America remained the leading regional market with a 37.0% share and USD 0.4 billion in revenue.

Service Type Analysis

The Subscription Model remained the leading service type, accounting for 61.4% of the market. Its strong position reflects the growing preference among commercial and industrial organizations for predictable operating expenses rather than large upfront capital investments. Subscription-based services combine battery hardware, software, maintenance, monitoring, and performance optimization into a single agreement, allowing businesses to focus on operations instead of system ownership. The model also provides continuous software updates and operational support, making it attractive for organizations seeking reliable energy management while reducing financial risks associated with purchasing battery storage systems outright.

Deployment Mode Analysis

The Behind-the-Meter (BTM) segment dominated the market with a 65.0% share. Businesses continue to adopt on-site battery energy storage systems to lower electricity costs, reduce peak demand charges, and improve overall energy efficiency. This deployment model enables commercial and industrial users to manage their own energy consumption more effectively while enhancing operational resilience during power disruptions. The flexibility and direct control offered by BTM systems have made them the preferred deployment option for organizations looking to optimize energy usage and improve long-term cost efficiency.

Enterprise Size Analysis

Large Enterprises led the market with a 68.5% share. Their financial strength allows them to adopt advanced battery energy storage technologies while supporting broader sustainability and energy efficiency initiatives. Industries including data centers, manufacturing, retail, and commercial real estate increasingly rely on energy storage as a service to optimize electricity consumption, reduce operational costs, and strengthen grid stability. Meanwhile, Small and Medium-sized Enterprises (SMEs) are emerging as an important customer segment as flexible subscription-based and pay-per-use business models make battery energy storage more accessible without requiring significant capital expenditure.

Industry Vertical Analysis

The Data Centers segment accounted for 35.6% of the market, making it the largest industry vertical. Growing cloud computing demand, expanding artificial intelligence workloads, and the rapid development of hyperscale digital infrastructure continue to increase the need for reliable backup power and uninterrupted energy supply. Battery energy storage solutions help data centers improve operational continuity while optimizing electricity consumption and reducing energy costs. The Retail and Hospitality segment also represents a significant portion of the market as shopping malls, hotels, and commercial buildings increasingly deploy battery storage systems for peak load management, energy cost optimization, and dependable backup power.

Key Market Segments

By Service Type

- Subscription Model

- Pay-Per-Use Model

- Others

By Deployment Mode

- Behind-the-Meter (BTM)

- Front-of-the-Meter (FTM)

By Enterprise Size

- Large Enterprises

- Small and Medium-sized Enterprises

By Industry Vertical

- Data Centers

- Retail and Hospitality

- Healthcare Facilities

- Others

Driving Factors

The market is primarily driven by expanding renewable energy integration mandates across major economies. China's National Energy Administration requires new renewable energy projects to include storage capacity equal to 10–20% of installed generation, creating an estimated 35 GWh of annual incremental storage demand by 2027. India's Solar Energy Corporation of India (SECI) has bundled 4 GWh of storage with 12 GW of solar capacity, while the National Electricity Plan (2023) projects battery energy storage requirements rising from 82 GWh in 2026–27 to 411 GWh by 2031–32. Australia's Capacity Investment Scheme (CIS) is also supporting contracted storage projects alongside a AUD 7.2 billion residential subsidy program. These policy initiatives are encouraging commercial and industrial customers to enter 10–15 year service agreements, creating long-term demand for Commercial Battery Energy Storage As a Service providers. Supporting this trend, global battery energy storage installations increased 61.3% to 275.3 GWh of new capacity in 2025, with 353.4 GWh projected for 2026, strengthening the pipeline for future service contracts.

Restraining Factors

Grid interconnection delays remain one of the most significant barriers to market expansion. By 2025, nearly 890 GW of storage capacity was waiting in U.S. interconnection queues, while the total queue exceeded 2.6 terawatts of generation and storage capacity. The average time between an interconnection request and commercial operation increased to nearly five years in 2023, compared with less than two years in 2008. During Tamarindo's March 2026 Investing in Battery Energy Storage Conference in London, 98% of industry participants identified grid connection delays as the largest project execution challenge, while 78% considered interconnection queues the primary regulatory obstacle across Europe. These delays can postpone project commissioning by 24–48 months, forcing service providers to renegotiate agreements, absorb contractual penalties, or lose customers while reducing expected project returns.

Growth Opportunity

A major opportunity for the market lies in integrating second-life EV batteries into commercial battery energy storage fleets. Batteries that fall below approximately 80% State of Health for automotive applications can be repurposed for stationary energy storage at an estimated USD 45–70/kWh, compared with USD 100–130/kWh for new LFP battery packs. Industry projections indicate that second-life battery capacity will expand from approximately 25–30 GWh in 2025 to 330–350 GWh by 2030, representing a nearly 65% CAGR. This cost advantage supports a two-tier pricing strategy in which premium contracts utilize new batteries while cost-sensitive customers are served using second-life battery systems. The approach can reduce total installed commercial battery system costs below USD 180/kWh, shorten payback periods to 4–5 years from 7–8 years, and expand adoption among retailers, logistics hubs, and educational institutions. Additionally, the EU Battery Regulation's Battery Passport requirement is expected to reduce battery screening costs from USD 15–25/kWh to below USD 3–5/kWh, improving sourcing efficiency and creating potential 15–20 margin point advantages for providers establishing early partnerships with automotive manufacturers.