Energy Management System Market Growth Scenario and Investment Opportunities

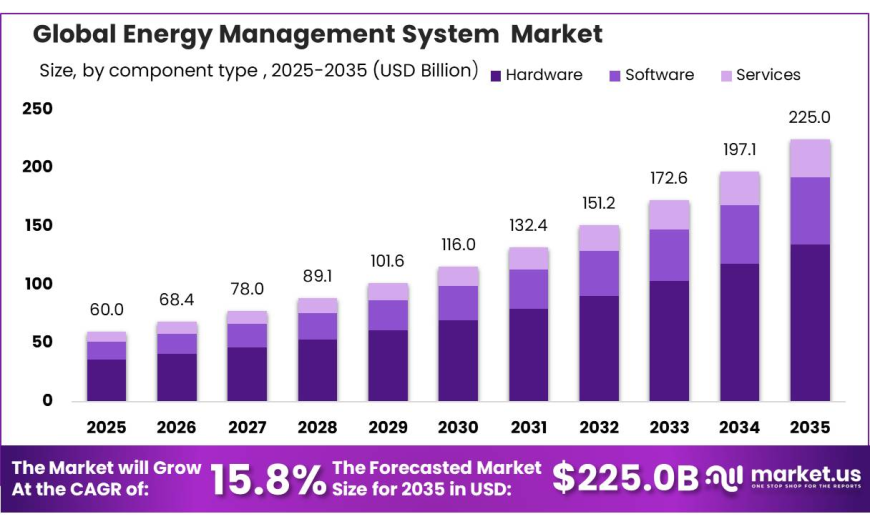

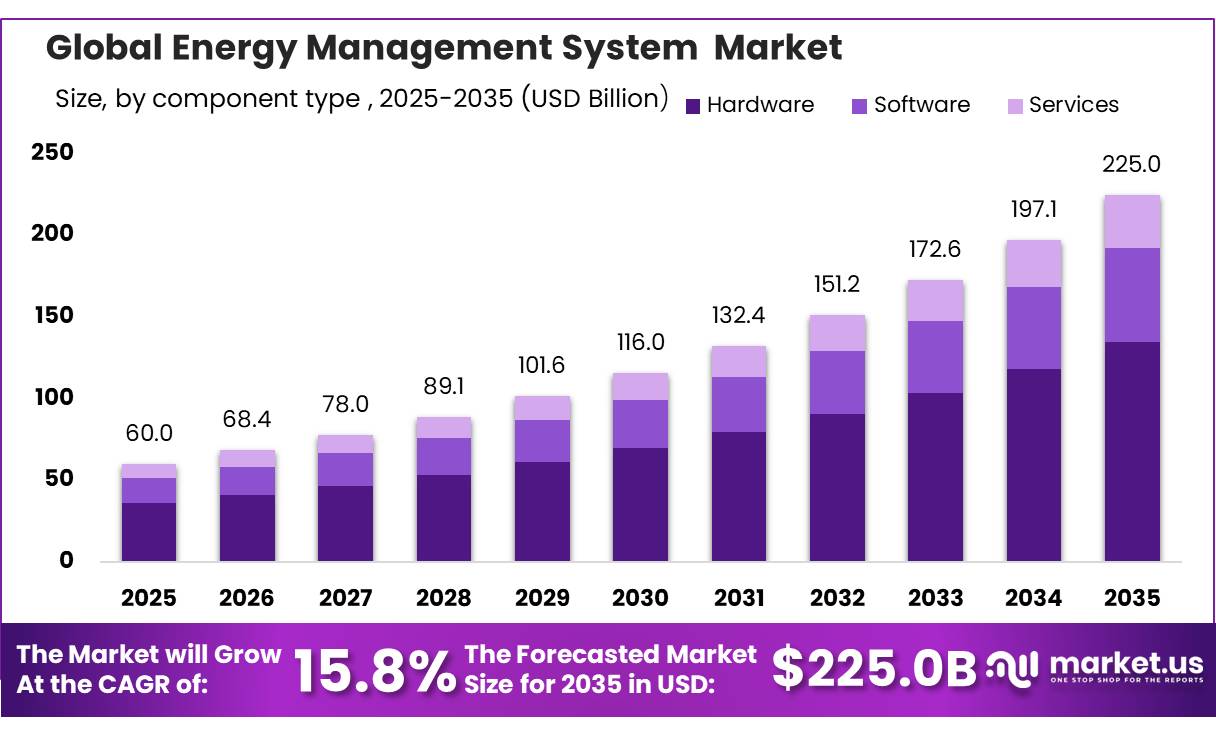

Explore the Energy Management System Market growth, trends, and forecast as the market reaches USD 225.0 billion by 2035 from USD 60.0 billion in 2025, registering a CAGR of 15.8%. Discover key segments, regional insights, growth drivers, challenges, and opportunities shaping energy efficiency and smart energy management adoption.

sonicbolt20

sonicbolt20

Overview

Energy Management System Market is positioned for strong growth as industries integrate intelligent systems to optimize energy usage and improve efficiency. The market size was recorded at USD 60.0 billion in 2025 and is expected to reach USD 225.0 billion by 2035, growing at a CAGR of 15.8% from 2026 to 2035. North America remained the dominant market with a 35.6% share, generating USD 21.36 Billion revenue. Expanding digital infrastructure and energy efficiency initiatives are driving EMS market development.

Key Takeaways

- The Energy Management System Market was valued at USD 60.0 billion in 2025.

- The market is expected to grow at a CAGR of 15.8% and reach USD 225.0 billion by 2035.

- The Hardware segment dominated the market, accounting for 60.0% of the total market share.

- The Industrial Energy Management System (IEMS) segment led the market with a 71.0% share.

- The Cloud-Based deployment segment held a leading position with 50.0% of the total market share.

- The Manufacturing sector accounted for 31.0% of the total market share among end-use industries.

- North America was the dominant region in 2024, capturing 35.6% of the market.

Energy Management System Market Segment

Component Analysis

The Hardware segment represents the dominant segment in the Energy Management System Market, accounting for 60.0% of total market share. Hardware components provide the essential infrastructure required for energy monitoring, data collection, and real-time consumption management across industrial, commercial, and residential environments. These solutions include smart meters, sensors, controllers, data loggers, display units, communication modules, and power monitoring devices that support effective energy management operations.

In February 2025, Honeywell International deployed advanced EMS hardware infrastructure through its Honeywell Building Management System platform, including smart sensors, controllers, and power monitoring devices for large-scale manufacturing and commercial building facilities.

Type Analysis

The Industrial Energy Management System (IEMS) segment dominates the EMS market, holding a 71.0% market share. IEMS solutions are widely adopted across manufacturing facilities, power and energy plants, oil and gas operations, and heavy industrial environments due to their ability to manage complex energy consumption requirements.

These systems provide real-time monitoring, automated demand response, and advanced data analytics capabilities that help organizations achieve measurable energy savings. In April 2025, Siemens AG deployed its Industrial Energy Management System across multiple large-scale manufacturing facilities, enabling real-time energy monitoring and automated demand response to support annual energy savings of up to 30%.

Deployment Mode Analysis

The Cloud-Based deployment segment holds a major position in the EMS market, accounting for 50.0% of the total market share. Cloud-based solutions offer flexibility, scalability, cost efficiency, and remote accessibility compared with traditional on-premises systems.

Organizations can monitor and optimize energy consumption across multiple locations through centralized digital platforms, reducing infrastructure requirements and improving operational control. The expansion of cloud computing, high-speed internet connectivity, and IoT integration has accelerated the adoption of cloud-based energy management solutions.

End-Use Industry Analysis

The Manufacturing sector represents a major segment in the EMS market, accounting for 31.0% of total market share. Manufacturing facilities are among the largest energy consumers due to continuous production operations, heavy machinery, HVAC systems, and extensive lighting infrastructure.

Energy Management Systems help manufacturing organizations analyze energy usage patterns, identify inefficiencies, optimize production schedules, utilize off-peak electricity rates, and automate responses to changing energy demands in real time.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Type

- Industrial Energy Management System (IEMS)

- Building Energy Management System (BEMS)

- Home Energy Management System (HEMS)

By Deployment Mode

- On-Premises

- Cloud-Based

- Hybrid Cloud

By End-Use Industry

- Manufacturing

- Power & Energy / Utilities

- Telecom & IT

- Commercial & Residential Buildings

- Healthcare & Hospitals

- Food & Beverage

- Others

Driving Factors

EU building-efficiency mandates driving EMS retrofits are creating strong demand for energy management solutions. The recast EPBD requires member states to transpose the directive by 29 May 2026, introduces minimum energy performance standards from 2026, mandates zero-emission public buildings from 2028 and all new buildings from 2030, and targets the worst-performing 16% of non-residential buildings by 2030 and 26% by 2033 for renovation action.

Smart-grid and AMI expansion, DER, solar, storage, and EV orchestration needs, industrial energy-cost pressure, AI analytics and cloud control, and carbon reporting requirements are also supporting EMS adoption across regions including North America, Europe, China, Japan, and Australia.

Restraining Factors

High upfront integration cost remains a key challenge for EMS adoption, particularly among SMEs and mid-market organizations. Typical EMS deployments for SMEs in 2026 require around US$20,000–80,000 of upfront integration and metering capex per site, along with US$4,000–25,000 in annual subscription opex.

Although EMS projects can deliver 10%–25% electricity savings and an additional 5%–10% bill reduction through load shifting, payback periods of approximately 2.5–4.5 years can delay investment decisions. Other challenges include legacy-system interoperability gaps, smart-meter rollout delays, cybersecurity and data-compliance requirements, retrofit disruption, and fragmented buyer ROI perception.

Growth Opportunity

VPP orchestration platforms represent a significant opportunity for EMS providers. The opportunity lies in moving beyond site-level monitoring and controls toward aggregating distributed assets into virtual power plants capable of coordinating solar, storage, EVs, CHP, and flexible loads.

The VPP market was around US$7.7 billion in 2026 by one estimate, with expansion supported by software that manages distributed energy resources in real time. EMS companies can expand revenue models through demand response, grid services, and flexibility-sharing opportunities. This approach could add an estimated +2.2 percentage points to CAGR in North America, Europe, Australia, and Japan where flexibility markets continue to develop.