Covered Stent Grafts and Advanced Devices Shape the Future of Aorto-Iliac Occlusive Disease Treatment

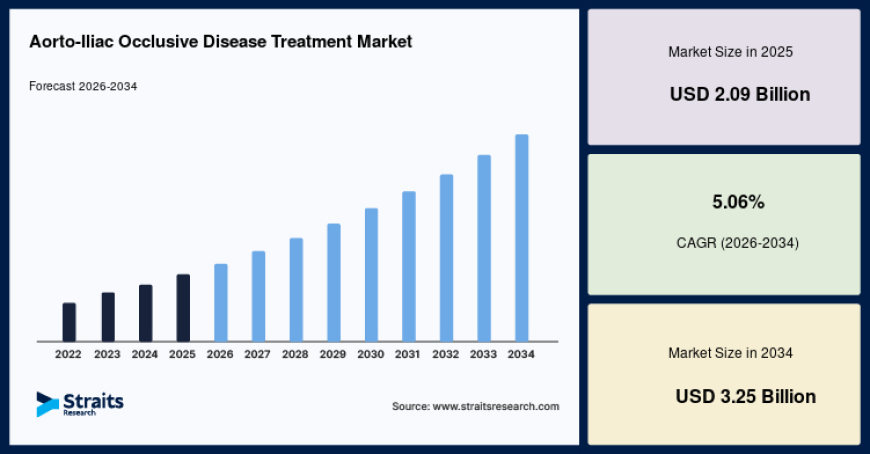

The global aorto-iliac occlusive disease treatment market size is valued at USD 2.09 billion in 2025 and is estimated to reach USD 3.25 billion by 2034, growing at a CAGR of 5.06% during the forecast period.

Aorto-Iliac Occlusive Disease Treatment Market

The global aorto-iliac occlusive disease treatment market is witnessing steady growth as healthcare systems increasingly focus on early diagnosis and intervention for peripheral arterial disease (PAD). Valued at USD 2.09 billion in 2025, the market is projected to reach USD 3.25 billion by 2034, expanding at a CAGR of 5.06% during the forecast period from 2026 to 2034.

Aorto-iliac occlusive disease is a form of peripheral arterial disease characterized by narrowing or blockage of the abdominal aorta and iliac arteries, leading to reduced blood flow to the lower extremities. Treatment approaches include a range of endovascular and surgical procedures designed to restore arterial patency, improve circulation, and reduce the risk of limb-threatening complications. The market encompasses endovascular devices, surgical instruments, procedural technologies, and specialized care settings involved in disease management.

Market Overview

The increasing global burden of peripheral arterial disease is creating sustained demand for advanced treatment solutions. Aging populations, rising rates of diabetes, smoking-related vascular disorders, and cardiovascular risk factors are contributing to higher incidence rates of aorto-iliac occlusive disease across both developed and emerging healthcare markets.

Clinical practice has increasingly shifted toward minimally invasive treatment approaches that offer shorter hospital stays, reduced recovery times, and lower procedural risks compared with traditional open surgery. As a result, endovascular interventions continue to account for a significant share of treatment procedures performed worldwide.

Healthcare providers are also investing in advanced imaging technologies, catheter-based interventions, and specialized vascular care programs, further supporting procedural volumes and market growth.

Growth Drivers

A key factor driving market expansion is the growing prevalence of peripheral arterial disease involving the aorto-iliac segment. Patients presenting with intermittent claudication, critical limb ischemia, and reduced lower-extremity perfusion increasingly require timely revascularization procedures to prevent disease progression and improve quality of life.

The widespread adoption of minimally invasive endovascular therapies has further accelerated market growth. Advances in stent technology, atherectomy systems, balloon angioplasty devices, and covered stent grafts have improved procedural success rates and expanded treatment options for complex lesions.

In addition, improved screening practices, including ankle-brachial index assessments and advanced vascular imaging, are enabling earlier diagnosis and intervention. These developments are supporting greater treatment accessibility and improved clinical outcomes across vascular care settings.

Emerging Market Trends

One of the most notable trends shaping the market is the shift from conventional iliac stenting toward lesion-specific endovascular solutions. Physicians increasingly select devices based on vessel anatomy, plaque morphology, calcification burden, and lesion complexity. This approach has encouraged wider adoption of covered stent grafts, bifurcated aortic stents, and specialized iliac platforms designed to address challenging anatomical conditions.

Another important trend is the growing use of image-guided procedural planning and staged revascularization strategies. Clinicians are increasingly utilizing intravascular imaging technologies and advanced diagnostic tools to improve procedural precision and optimize treatment outcomes. These structured treatment pathways support more efficient resource utilization while enhancing patient care.

The integration of hybrid treatment approaches that combine open surgery with endovascular techniques is also gaining traction, particularly for patients with complex multilevel arterial disease.

Market Challenges

Despite favorable growth prospects, several challenges continue to influence market development. One of the primary barriers involves reimbursement variability for complex aorto-iliac interventions. Procedures that involve multiple devices, adjunctive imaging technologies, and advanced treatment techniques often face inconsistent reimbursement frameworks across healthcare systems.

Administrative complexities related to coding and reimbursement can affect treatment planning and influence adoption rates for certain advanced procedures, particularly in cost-sensitive healthcare environments.

In addition, physician training requirements for complex interventions remain significant. Successful management of advanced aorto-iliac lesions often requires specialized expertise, limiting procedural availability in some regions and healthcare facilities.

Opportunities

The expansion of dedicated physician training programs presents a significant opportunity for market participants. Manufacturers and healthcare organizations are increasingly investing in simulation-based education, procedural workshops, and clinical support initiatives aimed at improving physician proficiency in complex vascular interventions.

Growing adoption of advanced endovascular technologies across emerging healthcare markets is expected to create additional opportunities for industry stakeholders. As healthcare infrastructure improves and access to specialized vascular care expands, demand for innovative treatment devices and procedural solutions is anticipated to increase.

The continued development of next-generation stent platforms, imaging-guided technologies, and integrated treatment systems is expected to further enhance procedural outcomes and support long-term market growth.

Regional Insights

North America remains the leading regional market, accounting for approximately 54% of global revenue in 2025. Strong adoption of catheter-based interventions, established vascular referral networks, and widespread utilization of advanced imaging technologies contribute to the region's dominant position.

The United States continues to represent the largest national market, supported by high awareness of peripheral arterial disease, routine vascular screening practices, and extensive availability of specialized treatment centers. The country's market was valued at USD 842.10 million in 2025, reflecting continued demand for both endovascular and surgical treatment approaches.

Asia Pacific is expected to record the fastest growth during the forecast period, supported by increasing diagnoses of peripheral arterial disease, expanding healthcare infrastructure, and growing access to vascular surgery services. Rising investments in interventional cardiology departments and increasing physician adoption of minimally invasive procedures are contributing to strong regional momentum.

China is emerging as a major growth market due to increasing use of vascular stents, expanding procedural expertise, and ongoing investments in advanced healthcare capabilities.

Europe continues to demonstrate steady growth, supported by established treatment protocols, favorable reimbursement frameworks, and close collaboration between vascular surgeons, interventional radiologists, and cardiovascular specialists. Germany remains one of the region's most important markets due to widespread vascular screening programs and strong adoption of advanced revascularization techniques.

Latin America and the Middle East & Africa are also witnessing gradual market expansion as healthcare providers continue to invest in vascular care infrastructure and advanced interventional capabilities.

Segment Analysis

By device type, endovascular devices dominated the market in 2025, supported by extensive use of balloon angioplasty systems, atherectomy devices, self-expanding stents, balloon-expandable stents, covered stent grafts, and bifurcated aortic stent grafts. Their compatibility with minimally invasive treatment strategies continues to drive adoption across healthcare facilities.

The surgical devices segment is expected to register notable growth during the forecast period, supported by the continued importance of open surgical reconstruction for patients with extensive or anatomically challenging disease.

Based on procedure type, endovascular procedures accounted for the largest share of market revenue, representing 63.24% of the market in 2025. The segment benefits from growing physician preference for minimally invasive interventions that offer reduced recovery times and lower procedural burden.

Hybrid procedures are anticipated to experience particularly strong growth as healthcare providers increasingly combine endovascular and open surgical techniques to address complex multilevel occlusive disease.

By end use, hospitals accounted for the largest share of market revenue, representing 50.23% in 2025. Access to advanced imaging technologies, multidisciplinary vascular teams, and specialized treatment capabilities continue to support hospital-based procedural volumes.

Outpatient facilities are expected to emerge as the fastest-growing end-use segment as selected endovascular procedures increasingly transition toward ambulatory care settings focused on efficiency and patient convenience.

Competitive Landscape

The global aorto-iliac occlusive disease treatment market remains moderately fragmented, with established cardiovascular device manufacturers competing alongside specialized vascular technology providers. Industry participants continue to focus on product innovation, physician education, clinical evidence generation, and procedural support programs to strengthen market positioning.

Key companies operating in the market include Medtronic plc, W. L. Gore & Associates, Inc., Boston Scientific Corporation, Abbott Laboratories, Cook Medical LLC, Terumo Corporation, Cordis Corporation, B. Braun Melsungen AG, BD, LeMaitre Vascular, Inc., Endologix, Inc., Inari Medical, Inc., Merit Medical Systems, Inc., Biotronik SE & Co. KG, and Meril Life Sciences Pvt. Ltd.

Recent industry developments have focused on expanding awareness initiatives, advancing endovascular treatment technologies, and improving procedural outcomes through innovative device platforms and physician training programs.

About the Market Study

The Aorto-Iliac Occlusive Disease Treatment Market report provides a comprehensive assessment of market dynamics, including growth drivers, emerging trends, competitive developments, regional performance, and future opportunities. The study analyzes historical market performance from 2022 to 2024 and provides forecasts through 2034. It covers device type, procedure type, end-use settings, and key regional markets to deliver strategic insights for healthcare providers, manufacturers, investors, and industry stakeholders.

Click to Read the Complete Insights & Report https://straitsresearch.com/report/aorto-iliac-occlusive-disease-treatment-market

About Straits Research

Straits Research is a global market research and consulting firm specializing in delivering actionable business intelligence, industry analysis, and market forecasting solutions. The company provides comprehensive research across healthcare, technology, consumer goods, industrial sectors, and emerging markets, helping organizations make informed strategic decisions through data-driven insights and market expertise.