Stationary Catalytic Systems Market Industry Overview and Forecast 2025–2034

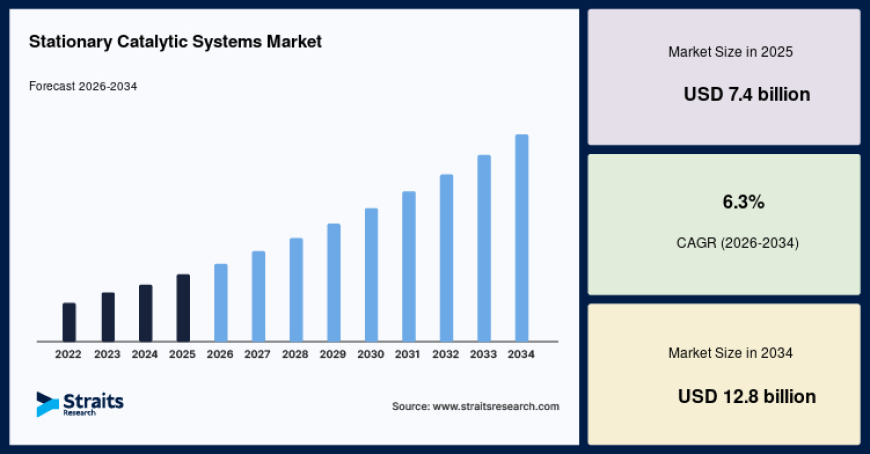

The global stationary catalytic systems market size is valued at USD 7.4 billion in 2025 and is projected to reach USD 12.8 billion by 2034, expanding at a CAGR of 6.3% during the forecast period.

Stationary Catalytic Systems Market

The global Stationary Catalytic Systems Market is witnessing significant expansion as industries worldwide prioritize emission reduction and sustainable manufacturing practices. The market is valued at USD 7.4 billion in 2025 and is projected to reach USD 12.8 billion by 2034, growing at a CAGR of 6.3% during the forecast period (2025–2034). The market growth is primarily driven by tightening environmental regulations, rising industrial emissions control requirements, continuous advancements in catalyst materials, and the increasing adoption of cleaner industrial processes across sectors such as power generation, chemicals, refining, and manufacturing.

Stationary catalytic systems are essential technologies used to reduce harmful emissions generated from industrial operations. These systems help industries comply with increasingly stringent environmental standards while improving process efficiency and reducing operational risks. As governments and regulatory agencies continue to impose strict emission norms, the demand for advanced catalytic solutions is expected to increase substantially over the coming years.

For detailed market insights, growth forecasts, and competitive analysis, visit: https://straitsresearch.com/report/stationary-catalytic-systems-market

Market Drivers

Stringent Environmental Regulations Fueling Market Growth

One of the primary drivers of the Stationary Catalytic Systems Market is the implementation of stringent environmental regulations across developed and developing economies. Governments worldwide are enforcing strict standards to control emissions of nitrogen oxides (NOx), sulfur oxides (SOx), volatile organic compounds (VOCs), and carbon monoxide from industrial facilities.

Industries are increasingly deploying stationary catalytic systems to ensure compliance with environmental laws and avoid regulatory penalties. Regulatory frameworks such as clean air initiatives and industrial emission directives are expected to continue supporting market expansion throughout the forecast period.

Rising Industrial Emission Control Requirements

Rapid industrialization and expanding manufacturing activities have significantly increased industrial emissions worldwide. Industries including power generation, oil and gas, petrochemicals, cement, and metals are under growing pressure to reduce their environmental footprint.

Stationary catalytic systems provide an efficient solution for minimizing harmful emissions while maintaining operational productivity. The increasing emphasis on sustainable industrial operations and environmental responsibility is expected to accelerate product adoption globally.

Advancements in Catalyst Technologies

Continuous innovations in catalyst materials and system designs are contributing significantly to market growth. Manufacturers are developing advanced catalyst formulations with improved efficiency, durability, and resistance to contamination.

Technological advancements such as enhanced precious metal catalysts, zeolite-based catalysts, and improved selective catalytic reduction technologies are helping industries achieve higher emission reduction rates while lowering maintenance requirements. These innovations are expected to create new growth opportunities for market participants.

Market Challenges

High Installation and Operational Costs

Despite strong growth prospects, high installation and maintenance costs remain a significant challenge for the Stationary Catalytic Systems Market. Implementing catalytic systems often requires substantial capital investment, particularly for large industrial facilities.

In addition to installation expenses, industries must also incur recurring costs related to catalyst replacement, system maintenance, and performance monitoring. These financial constraints may limit adoption among small and medium-sized enterprises.

Catalyst Deactivation and Performance Degradation

Catalyst performance can deteriorate over time due to factors such as thermal degradation, poisoning, fouling, and exposure to contaminants. Deactivated catalysts may reduce emission control efficiency and increase operational downtime.

To overcome this challenge, manufacturers are investing heavily in research and development activities to improve catalyst lifespan and operational reliability. However, catalyst degradation continues to pose a major concern for industrial operators.

Complex Regulatory Landscape

Environmental regulations vary considerably across countries and regions, creating challenges for system manufacturers and end users. Companies operating globally must customize their solutions to meet specific regional requirements, increasing complexity and operational costs.

The evolving nature of environmental policies also necessitates continuous product innovation and compliance monitoring.

Market Segmentation

By Type

The market is segmented into:

- Selective Catalytic Reduction (SCR) Systems

- Oxidation Catalytic Systems

- Reforming and Process Catalysts

- Three-Way Catalytic Systems

- Others

Selective Catalytic Reduction systems hold the largest market share owing to their exceptional efficiency in reducing NOx emissions from industrial combustion processes. Their widespread use in power plants and heavy industries continues to drive segment growth.

Oxidation catalytic systems are anticipated to witness substantial growth during the forecast period due to increasing demand for VOC and carbon monoxide emission control across industrial applications.

By Application

The market is segmented into:

- NOx Reduction

- VOC and CO Oxidation

- Sulfur Compound Control

- Process Efficiency Enhancement

NOx reduction dominates the application segment as governments continue implementing strict nitrogen oxide emission standards for industrial facilities.

VOC and CO oxidation is projected to emerge as the fastest-growing application segment due to increasing awareness regarding air quality improvement and industrial sustainability initiatives.

By End User

The major end-user industries include:

- Power Generation

- Oil and Gas Refining

- Chemical Manufacturing

- Cement Industry

- Metals and Mining

- Pulp and Paper

- Others

Power generation represents the dominant end-user segment. Thermal power plants extensively utilize stationary catalytic systems to meet emission standards and improve operational efficiency.

Chemical manufacturing is expected to experience rapid growth owing to increasing production capacities, stringent environmental norms, and growing investments in sustainable manufacturing technologies.

Regional Insights

North America

North America holds a significant share of the Stationary Catalytic Systems Market due to stringent environmental regulations and well-established industrial infrastructure. The United States remains a key contributor owing to strong regulatory enforcement and growing investments in emission control technologies.

Increasing modernization of aging industrial facilities and rising demand for cleaner energy generation are expected to support regional market growth.

Europe

Europe is one of the leading regional markets, driven by ambitious climate goals and strict emission reduction policies. Countries such as Germany, France, and the United Kingdom are actively investing in industrial decarbonization initiatives.

The widespread adoption of advanced catalytic technologies across manufacturing and power generation sectors continues to strengthen the European market position.

Asia-Pacific

Asia-Pacific is expected to register the fastest growth during the forecast period. Rapid industrialization, expanding energy demand, and increasing environmental awareness are driving market expansion across China, India, Japan, and South Korea.

Growing investments in industrial infrastructure, coupled with stricter environmental regulations, are creating lucrative opportunities for market participants in the region.

Latin America, Middle East, and Africa

The Latin America, Middle East, and Africa region is experiencing steady growth due to increasing industrial activities and rising investments in energy and manufacturing sectors.

The expansion of oil and gas refining operations, mining projects, and power generation facilities is expected to drive demand for stationary catalytic systems across these regions.

Key Players Analysis

The Stationary Catalytic Systems Market is moderately competitive, with major companies focusing on technological innovation, strategic collaborations, mergers and acquisitions, and product portfolio expansion to strengthen their market presence.

Leading players are increasingly investing in advanced catalyst technologies to improve system efficiency, reduce emissions, and meet evolving regulatory requirements.

Key companies operating in the market include:

- Johnson Matthey

- BASF SE

- Haldor Topsoe A/S

- Honeywell International Inc.

- CECO Environmental

- GE Vernova

- Babcock & Wilcox Enterprises Inc.

- Clariant AG

- MAN Energy Solutions

- DuPont

- Shell Catalysts & Technologies

- Cormetech Inc.

Conclusion

The Stationary Catalytic Systems Market is poised for sustained growth through 2034, supported by tightening environmental regulations, rising industrial emission control requirements, and continuous technological advancements. Although challenges such as high installation costs and catalyst degradation persist, ongoing innovations and increasing adoption of sustainable industrial processes are expected to create significant growth opportunities. As industries continue prioritizing environmental compliance and operational efficiency, demand for stationary catalytic systems will remain strong worldwide.

About Us

Straits Research is a leading market research and intelligence organization specializing in research, analytics, and advisory services. The company provides comprehensive market reports, industry insights, and strategic business intelligence across multiple industries, helping organizations identify growth opportunities and make informed business decisions.

Contact Us

Email: [email protected]

Tel: +1 646 905 0080 (U.S.)

Tel: +44 203 695 0070 (U.K.)