Loan Management System: A Step-by-Step Guide for Banks and NBFCs

Discover how a Loan Management System streamlines loan origination, underwriting, disbursement, repayment, and collections for banks and NBFCs. Learn key features, benefits, and implementation steps.

The financial services industry is undergoing rapid digital transformation, and traditional lending processes are no longer sufficient to meet growing customer expectations. Banks and Non-Banking Financial Companies (NBFCs) are increasingly adopting technology-driven solutions to automate operations, reduce manual errors, and improve customer experiences.

One of the most essential technologies in this transformation is a Loan Management System (LMS). It enables lenders to manage the complete loan lifecycle—from customer onboarding and application processing to loan disbursement, EMI tracking, collections, and loan closure.

For financial institutions looking to improve operational efficiency and remain competitive, implementing a robust Loan Management System is no longer optional—it's a necessity.

This comprehensive guide explains everything banks and NBFCs need to know about Loan Management Systems, including their features, benefits, implementation process, and best practices.

What is a Loan Management System?

A Loan Management System (LMS) is software designed to automate and streamline every stage of the lending process.

Instead of managing loans manually through spreadsheets or disconnected software, an LMS provides a centralized platform that handles:

- Loan applications

- Customer verification

- Credit assessment

- Approval workflows

- Loan disbursement

- EMI calculations

- Payment tracking

- Collections management

- Regulatory reporting

- Customer communication

The system significantly reduces paperwork while improving speed, transparency, and compliance.

Why Banks and NBFCs Need a Loan Management System

Manual loan processing often results in:

- Slow approvals

- Human errors

- Data duplication

- Compliance risks

- Higher operational costs

- Poor customer experience

A modern Loan Management System solves these challenges through automation and intelligent workflows.

Benefits include:

- Faster loan approvals

- Reduced processing costs

- Improved borrower experience

- Better portfolio management

- Enhanced compliance

- Real-time reporting

- Automated collections

- Reduced default risks

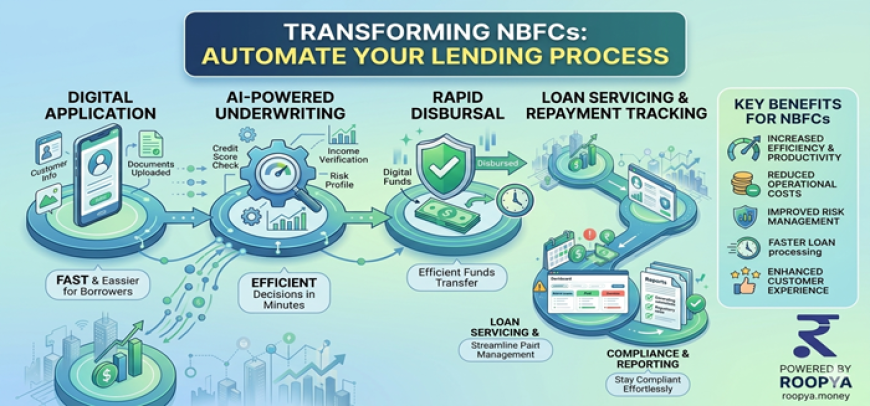

Step 1: Customer Onboarding

The lending journey begins with customer onboarding.

An advanced Loan Management System enables digital onboarding through:

- Online application forms

- Mobile-based registration

- Aadhaar verification

- PAN validation

- Digital document upload

- Video KYC

- eSign integration

The process minimizes paperwork while ensuring faster customer acquisition.

Step 2: Loan Application Processing

Once customer information is collected, the system validates submitted data automatically.

Key activities include:

- Personal information verification

- Employment verification

- Income validation

- Business verification

- Bank statement analysis

- Document authentication

Automation eliminates repetitive manual work and accelerates approvals.

Step 3: Credit Assessment and Risk Analysis

Before approving any loan, lenders must evaluate borrower risk.

Modern Loan Management Systems integrate with:

- Credit bureaus

- Alternative data providers

- Banking APIs

- Financial analytics tools

Risk scoring models evaluate:

- Credit history

- Existing liabilities

- Repayment behavior

- Income stability

- Debt-to-income ratio

This enables lenders to make informed decisions while minimizing defaults.

Step 4: Automated Loan Approval Workflow

Instead of relying solely on manual review, intelligent workflows automate approval processes.

Approval rules may include:

- Credit score thresholds

- Loan amount limits

- Income criteria

- Business rules

- Risk grades

Applications meeting predefined conditions can be approved instantly, while exceptional cases are routed to underwriters.

Step 5: Loan Disbursement

After approval, the Loan Management System automates fund disbursement.

The system generates:

- Loan agreements

- Digital contracts

- Sanction letters

- Payment instructions

Funds are transferred electronically to customer bank accounts with complete transaction records.

Step 6: EMI Scheduling and Repayment Management

Repayment tracking is one of the most important functions of an LMS.

The software automatically creates repayment schedules based on:

- Loan tenure

- Interest rate

- EMI frequency

- Principal amount

Borrowers receive reminders through:

- SMS

- Mobile notifications

The system updates repayment status in real time.

Step 7: Collection Management

Late payments can impact portfolio performance significantly.

An advanced Loan Management System includes automated collection workflows.

Features include:

- Payment reminders

- Overdue alerts

- Collection assignments

- Escalation rules

- Field collection tracking

- Settlement management

Automation improves recovery rates while reducing collection costs.

Step 8: Portfolio Monitoring

Banks and NBFCs manage thousands of active loans simultaneously.

An LMS provides dashboards showing:

- Total loan portfolio

- Active loans

- Delinquent accounts

- Non-performing assets (NPAs)

- Recovery rates

- Collection efficiency

- Revenue trends

Real-time insights help management make better business decisions.

Step 9: Compliance and Regulatory Reporting

Financial institutions operate under strict regulatory frameworks.

Loan Management Systems simplify compliance by maintaining complete audit trails and generating reports required by regulators.

Compliance capabilities include:

- KYC monitoring

- AML checks

- Audit logs

- Data security controls

- Regulatory reporting

- Digital record management

This reduces compliance risks while improving transparency.

Step 10: Loan Closure and Customer Retention

After successful repayment, the system automatically:

- Marks loans as closed

- Generates No Due Certificates

- Releases collateral

- Updates customer history

- Maintains digital records

Satisfied borrowers can then be targeted for cross-selling or repeat lending opportunities.

Key Features of a Modern Loan Management System

End-to-End Loan Lifecycle Management

Manages the entire lending process from application to closure.

Automated Workflow Engine

Reduces manual intervention through configurable business rules.

Digital KYC Integration

Supports Aadhaar, PAN, OCR, and document verification.

Multi-Product Lending

Supports:

- Personal Loans

- Business Loans

- Gold Loans

- Vehicle Loans

- MSME Loans

- Education Loans

- Consumer Durable Loans

Credit Bureau Integration

Provides real-time credit checks for faster decision-making.

Payment Gateway Integration

Supports automated EMI collection through multiple payment channels.

Collection Management

Improves recovery using automated reminders and field collection tools.

Analytics Dashboard

Offers real-time business intelligence and portfolio monitoring.

API Integration

Connects seamlessly with banking systems, CRMs, accounting software, and fintech platforms.

Cloud Deployment

Enables secure, scalable, and remote operations.

Benefits for Banks

Banks benefit from:

- Faster loan processing

- Reduced paperwork

- Improved operational efficiency

- Better risk management

- Higher compliance

- Enhanced customer satisfaction

- Lower operational costs

Benefits for NBFCs

NBFCs often require greater flexibility and speed.

A Loan Management System helps them by:

- Launching new lending products quickly

- Scaling operations efficiently

- Automating underwriting

- Managing collections effectively

- Reducing turnaround time

- Improving profitability

How AI is Transforming Loan Management Systems

Artificial Intelligence is redefining lending operations.

Modern LMS platforms use AI for:

- Automated credit scoring

- Fraud detection

- Predictive analytics

- Collection prioritization

- Customer behavior analysis

- Document extraction

- Chatbot support

These capabilities improve accuracy while reducing operational risks.

Choosing the Right Loan Management System

Before selecting an LMS, lenders should evaluate:

Scalability

Can the platform handle future business growth?

Customization

Can workflows be tailored to business requirements?

Security

Does it provide enterprise-grade security and encryption?

Integration

Can it connect with existing banking infrastructure?

Regulatory Compliance

Does it support RBI and industry compliance requirements?

Cloud Support

Does it offer secure cloud deployment and disaster recovery?

Analytics

Does it provide actionable reporting and dashboards?

Best Practices for Successful LMS Implementation

- Clearly define business requirements.

- Map existing lending workflows.

- Train employees thoroughly.

- Integrate with existing systems.

- Test workflows before deployment.

- Ensure strong cybersecurity measures.

- Continuously monitor system performance.

- Regularly update compliance rules.

Future of Loan Management Systems

The future of lending is digital-first.

Emerging technologies such as AI, Machine Learning, Open Banking APIs, Blockchain, and Predictive Analytics will continue transforming Loan Management Systems.

Banks and NBFCs that adopt intelligent automation today will be better positioned to improve customer satisfaction, reduce costs, and stay competitive in the rapidly evolving financial ecosystem.

A Loan Management System is more than just software—it is the backbone of modern digital lending.

By automating loan origination, underwriting, repayment management, collections, and compliance, banks and NBFCs can significantly improve efficiency while delivering exceptional customer experiences.

As digital lending continues to grow, investing in a scalable and intelligent Loan Management System will become a key competitive advantage for financial institutions seeking sustainable growth and operational excellence.

(FAQs)

1. What is a Loan Management System?

A Loan Management System is software that automates the complete loan lifecycle, including application processing, approval, disbursement, repayment tracking, collections, and closure.

2. How does a Loan Management System help NBFCs?

It reduces manual work, speeds up loan approvals, improves compliance, automates collections, and enhances customer experience.

3. Can banks customize a Loan Management System?

Yes. Modern platforms allow customization of workflows, approval rules, products, and reporting based on business needs.

4. Is a cloud-based Loan Management System secure?

Most enterprise-grade cloud LMS platforms use advanced encryption, role-based access controls, backups, and security protocols to protect sensitive financial data.

5. Does a Loan Management System support digital KYC?

Yes. Most modern solutions integrate with Aadhaar verification, PAN validation, OCR, eKYC, and digital document management.

6. Can the system automate EMI reminders?

Yes. Automated SMS, email, WhatsApp, and mobile notifications can remind borrowers about upcoming or overdue payments.

7. Is AI used in Loan Management Systems?

Yes. AI helps with credit scoring, fraud detection, predictive analytics, document processing, and automated decision-making.

8. Why should banks invest in a Loan Management System?

It improves operational efficiency, reduces costs, enhances customer satisfaction, strengthens compliance, and enables scalable digital lending.