Switching to Roopya: Benefits Every NBFC Should Know

Discover why NBFCs across India are switching to Roopya's no-code lending platform. Faster go-live, lower costs, 300+ integrations, AI decisioning & full RBI compliance.

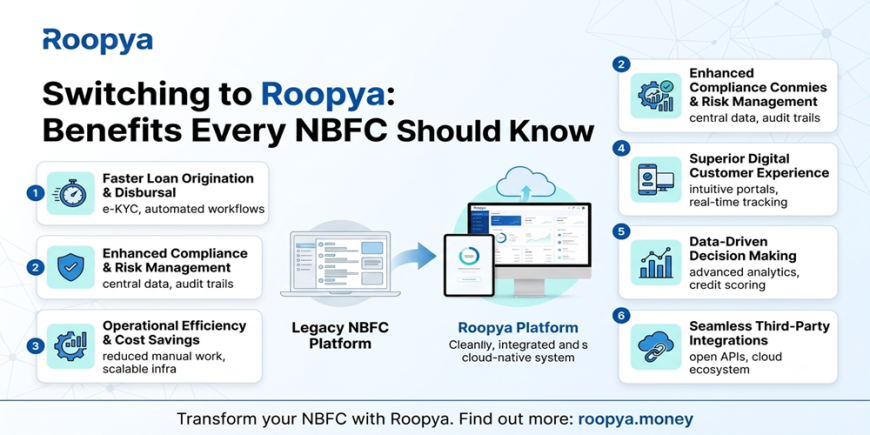

Running an NBFC in India today means navigating a landscape that is more competitive, more regulated, and more digital than ever before. Borrowers expect instant decisions. Regulators demand complete audit trails. Investors want scalable operations with manageable costs. And your competitors — many of them born-digital fintech lenders — are already operating at a speed and efficiency that legacy software simply cannot match.

If your NBFC is still running on a patchwork of outdated software, manual spreadsheets, or an on-premise loan management system that takes months to update, you already know the pain points: slow disbursements, compliance anxiety, expensive IT overheads, and an inability to launch new loan products without writing months of code.

This is exactly why hundreds of NBFCs across India are making the move to Roopya — a purpose-built, no-code digital lending platform that gives you enterprise-grade lending infrastructure from day one, without the enterprise-level price tag or the endless implementation timeline.

Here is everything you need to know about what changes — and what improves — when your NBFC switches to Roopya.

1. Go Live in 1 Day — Not 6 Months

One of the most common frustrations NBFC leaders share about traditional lending software is time-to-value. Implementations that were promised in eight weeks stretch to six months. Customisation requests pile up in a vendor backlog. By the time the system goes live, the market has shifted.

Roopya is engineered to eliminate this problem entirely. T

he platform ships with 20+ pre-configured loan product journeys — personal loans, business loans, MSME credit, gold loans, microfinance, and more — that are ready to use on day one. There is no complex installation, no server provisioning, and no months-long configuration cycle.

Most NBFCs that switch to Roopya are processing live loan applications within 24 hours of signing up. That is not a marketing claim — it is the architecture. Because Roopya is a cloud-native, no-code platform, setup is a matter of configuration, not construction.

2. No-Code Control — Your Team Runs the Platform, Not Your IT Vendor

Legacy lending software creates a dangerous dependency: every change to a credit policy, every new product parameter, every workflow adjustment requires a developer or a support ticket to the vendor. This means your business is always waiting on someone else to implement what your risk team decided last week.

Roopya breaks this dependency completely. The platform is built on a true no-code architecture, meaning your credit managers, operations leads, and product owners can make changes directly — through intuitive dashboards and drag-and-drop interfaces — without touching a single line of code.

Want to change your minimum CIBIL score threshold for a personal loan product? Done in minutes. Want to add a new geographic restriction to a business loan portfolio? Configure it in the Business Rule Engine and it goes live immediately. Want to create an entirely new loan product for a new borrower segment? Use a pre-built template and customise it yourself.

This is not just a convenience — it is a fundamental shift in how your NBFC operates. Your team becomes the owner of your lending technology, not just a user of it.

3. 300+ Pre-Built Integrations — Ready on Day One

Modern NBFC operations depend on a complex ecosystem of third-party services: credit bureaus, KYC providers, eSign platforms, bank account verification services, GST data providers, accounting software, payment gateways, and more. Building and maintaining these integrations in-house is expensive, time-consuming, and a constant source of technical debt.

When you switch to Roopya, you inherit 300+ pre-built, production-ready integrations from day one. This includes:

● All four major credit bureaus: CIBIL, Experian, Equifax, and CRIF — with automated report pulling and parsing.

● Complete KYC stack: Aadhaar eKYC, PAN verification, Digilocker, VKYC, and CKYC — fully integrated and RBI-compliant.

● eSign providers: Aadhaar OTP-based and Digilocker-based eSign for legally valid, paperless loan agreement execution.

● Bank account verification: Penny drop, bank statement analysis via Account Aggregator, and NACH/eNACH mandate registration.

● GST and ITR data: Direct GST portal integration and ITR data pulls for income verification of self-employed and MSME borrowers.

● Payment gateways and disbursement APIs: For instant, automated disbursement post-sanction.

Every one of these integrations is maintained, monitored, and updated by Roopya's engineering team — so you are never chasing a broken API or scrambling to meet a vendor's deprecation deadline.

4. AI-Powered Credit Decisioning — Faster, Smarter, and More Consistent

Credit decisioning is where the most value is created — and where the most risk lives — in any NBFC. Manual underwriting is slow, expensive, and inconsistent. Different underwriters apply different judgements to similar profiles, creating portfolio-level unpredictability.

Roopya's AI-powered decisioning engine changes this. The platform's Business Rule Engine (BRE) allows you to codify your credit policy precisely — every variable, every threshold, every exception — and apply it uniformly to every single application, automatically. No human inconsistency. No missed policy steps. No bias.

On top of the rule engine, Roopya's machine learning models analyse hundreds of data signals — bureau data, bank statement patterns, GST filing history, employment stability, geographic risk factors — to generate a holistic credit score that goes far beyond a simple CIBIL number. This means you can lend more confidently to thin-file borrowers and new-to-credit segments that traditional underwriting approaches systematically underserve.

The result: faster decisions (seconds, not days), lower credit costs, better portfolio quality, and the ability to serve a broader borrower base without taking on unmanaged risk.

5. RBI Compliance Built In — Not Bolted On

Regulatory compliance is one of the most resource-intensive functions in any NBFC. KYC documentation, PMLA compliance, credit bureau reporting, CERSAI registration, Fair Practice Code adherence, digital consent management — the list is long and the consequences of getting it wrong are severe.

Roopya is built with compliance as a first principle, not an afterthought. Every loan application processed on the platform automatically generates a complete, timestamped audit trail. Digital consent is captured and stored at every stage. Bureau reporting is automated. CERSAI filings are integrated. KYC processes are pre-validated against RBI norms.

Crucially, Roopya's compliance layer is continuously updated as regulations evolve. When the RBI issues new guidelines — on digital lending, KYC norms, or data localisation — Roopya updates the platform proactively. Your NBFC stays compliant without your team having to monitor every regulatory circular and implement changes in legacy code.

6. Scale Without Adding Headcount

Growth is the goal of every NBFC — but growth in a manual or legacy-software environment means proportional headcount growth. More applications mean more underwriters, more operations staff, more compliance reviewers. The unit economics deteriorate exactly when you want them to improve.

Roopya's cloud-native architecture scales horizontally without additional operational overhead. Whether your monthly disbursement volume is ₹1 crore or ₹500 crore, the platform handles the load automatically. There are no server upgrades to plan, no capacity constraints to manage, and no performance degradation during peak periods.

Automation handles the repetitive, high-volume tasks — KYC verification, document checking, bureau pulls, eligibility screening — freeing your human teams to focus on exception handling, customer relationships, and strategic decisions. This means you can grow your loan book significantly without a proportional increase in operational costs.

7. Pay-As-You-Use Pricing — Aligned With Your Growth

Traditional lending software is typically sold on a large upfront licence fee model, often accompanied by expensive annual maintenance contracts and per-module pricing that quickly adds up. For an NBFC at an early or mid-growth stage, this represents a significant capital outlay before a single loan is processed.

Roopya operates on a pay-as-you-use model with zero upfront licence costs. You pay based on actual usage — the number of applications processed, loans disbursed, or API calls made — meaning your technology cost scales directly with your revenue. When volumes are lower, your costs are lower. As you grow, the platform grows with you.

This pricing model fundamentally changes the economics of lending technology. It makes Roopya accessible to a newly licensed NBFC on day one, and it remains competitive as that same NBFC scales to hundreds of crores in monthly disbursements.

8. Multi-Product, Multi-Channel From a Single Platform

Most NBFCs do not operate a single loan product through a single channel. You may have a personal loan product for salaried borrowers, an MSME credit line for small businesses, and a gold loan product for rural borrowers — all originated through a mix of direct digital, DSA, and branch channels.

Managing multiple products through multiple channel-specific systems creates data silos, reporting complexity, and operational fragmentation. Roopya solves this by providing a unified platform that manages all your products and all your channels from a single operational dashboard.

Product-specific credit policies, workflows, pricing rules, and documentation requirements are all configurable independently within the same platform. Channel-specific reporting and incentive tracking for DSAs are built in. Your entire lending operation — across products and channels — becomes visible and manageable from one place.

9. Faster Collections and Better Borrower Experience

The borrower relationship does not end at disbursement. Collections, repayment management, and customer communication are equally important to portfolio health and NBFC reputation. Roopya's integrated Loan Management System (LMS) ensures the post-disbursement experience is as smooth as the application journey.

Automated repayment reminders via SMS, WhatsApp, and email reduce delinquency rates. NACH and eNACH mandate management ensures timely collections without manual follow-up. Borrower self-service portals allow customers to check outstanding balances, download statements, and raise service requests — reducing inbound support volume significantly.

10. Trusted by India's Modern Lenders

Roopya is not a new entrant still finding its product-market fit. The platform is trusted by a growing roster of modern Indian lenders — including IndiaKaLoan, QuickFinShop, Recapita, Findoc, and EazyCredit — who have switched to Roopya and experienced measurable improvements in processing speed, operational efficiency, and portfolio quality.

When you switch to Roopya, you join a network of lenders that collectively process thousands of loan applications daily on the platform. That scale translates into continuous product improvement, robust infrastructure reliability, and a vendor that is deeply invested in the success of the Indian NBFC ecosystem.

Making the Switch: What the Transition Looks Like

A common concern when switching lending platforms is data migration and transition risk. Roopya's onboarding team manages the transition process end to end — from data migration planning to parallel-run testing to go-live sign-off. Most NBFCs complete the transition with zero disruption to live lending operations.

The no-code architecture means your team can be trained and independently operating the platform within days, not weeks. And because Roopya's infrastructure is cloud-hosted, there is no hardware decommissioning, no on-premise software uninstallation, and no server room to manage.

If you are ready to explore what switching to Roopya would look like for your NBFC, the team offers a personalised demo, a no-obligation trial, and a migration assessment at no cost. Go live in a day. Grow without limits.

————————————————————————————————————————————————————————————

FREQUENTLY ASKED QUESTIONS (FAQ)

Q1: Why should my NBFC switch to Roopya?

Roopya gives your NBFC enterprise-grade lending infrastructure — no-code LOS, 300+ pre-integrated APIs, AI credit decisioning, and full RBI compliance — with a 1-day go-live and pay-as-you-use pricing. It replaces slow, expensive legacy systems with a platform built specifically for the Indian lending market.

Q2: How difficult is it to switch from our current lending software to Roopya?

Roopya's onboarding team manages the entire transition — including data migration, parallel-run testing, and go-live support. Most NBFCs complete the switch without any disruption to live lending operations. The no-code platform means your team can be independently operating within days of go-live.

Q3: How long does it take to go live on Roopya after switching?

Most NBFCs are processing live loan applications within 24 hours of completing onboarding. Pre-configured product journeys and plug-and-play integrations eliminate the lengthy implementation cycles typical of traditional lending software.

Q4: Will we lose any data when switching to Roopya?

No. Roopya's onboarding team conducts a structured data migration process, transferring your existing loan portfolio, borrower records, and historical data to the new platform with full integrity checks before go-live.

Q5: Is Roopya suitable for small or newly licensed NBFCs?

Absolutely. Roopya's pay-as-you-use pricing model means there are zero upfront licence costs, making it equally accessible for a newly licensed NBFC processing its first loans and a large NBFC disbursing hundreds of crores per month.

Q6: How does Roopya handle RBI compliance requirements?

Compliance is built into the platform at every layer — automatic KYC validation, digital consent capture, timestamped audit trails, automated bureau reporting, and CERSAI integration. Roopya's compliance layer is continuously updated whenever RBI issues new guidelines, so your NBFC stays compliant without manual intervention.

Q7: Can Roopya handle all our loan products from a single platform?

Yes. Roopya supports 20+ pre-configured loan product journeys — personal loans, business loans, MSME credit, gold loans, home loans, payday loans, auto loans, microfinance, and more — all manageable from a single operational dashboard with product-specific configurations.

Q8: What integrations come with Roopya out of the box?

Roopya ships with 300+ pre-built integrations including all four credit bureaus (CIBIL, Experian, Equifax, CRIF), full KYC stack (Aadhaar eKYC, PAN, Digilocker, VKYC), eSign providers, payment gateways, GST data, ITR data, Account Aggregator, NACH/eNACH, and accounting software.

Q9: Does switching to Roopya require hiring a technical team?

No. Roopya is a true no-code platform, meaning your credit managers, operations leads, and product owners can configure and manage the platform independently — without developers or technical staff. Changes to credit policies, workflows, and product parameters are made through intuitive dashboards, not code.

Q10: How is Roopya priced?

Roopya uses a pay-as-you-use model with zero upfront licence fees. Your cost scales directly with your usage — the number of applications processed, loans disbursed, or API calls made — making it economically aligned with your growth at every stage.