Carbon Capture and Storage Market Commercialization Trends in Large Scale CCS Projects

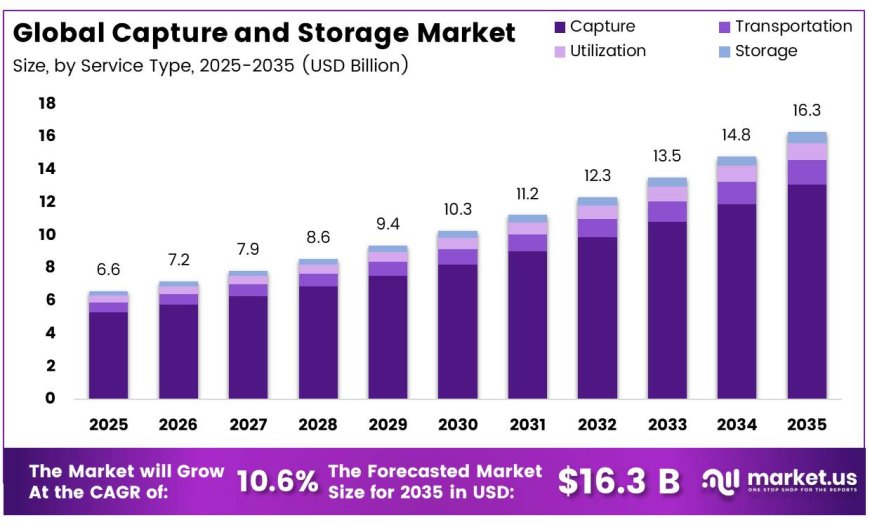

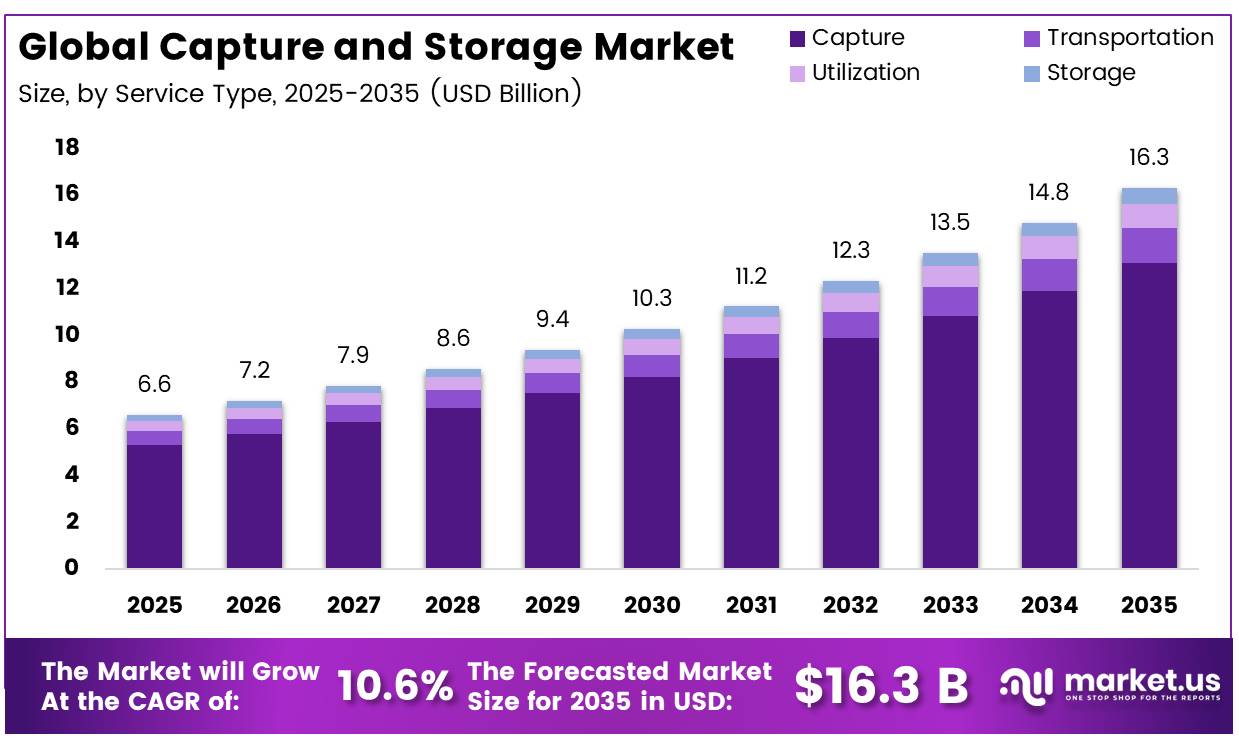

Carbon Capture and Storage Market is projected to grow from USD 6.6 billion in 2025 to USD 16.3 billion by 2035, registering a CAGR of 10.6 https://market.us/report/carbon-capture-and-storage-market/

sonicbolt20

sonicbolt20

Overview

The Carbon Capture and Storage Market continues to gain momentum as governments and industries focus on reducing industrial carbon emissions. The market was valued at USD 6.6 billion in 2025 and is anticipated to reach USD 16.3 billion by 2035, recording a CAGR of 10.6%. North America led the global market with a 45.80% share and USD 3.02 billion in revenue, supported by favorable policies, infrastructure development, and investments in carbon management projects.

Key Takeaways

- The Global Carbon Capture and Storage Market was valued at USD 6.6 billion in 2025.

- The market is expected to reach USD 16.3 billion by 2035, expanding at a CAGR of 10.6% during 2025–2035.

- Capture led the market by service, accounting for 80.30% of the total market share.

- Post-Combustion Capture dominated the technology segment with a 50.00% market share.

- Point Source Capture (Industrial Stacks) held the leading position among capture sources, representing 84.50% of the market.

- The Oil & Gas industry accounted for 42.00% of the total market among end-use industries.

- North America remained the leading regional market with a 45.80% share.

Capture and Storage Market Segmentation

Service Analysis

Capture remained the dominant service segment in 2025, holding more than 80.30% of the market. Carbon dioxide must first be separated from industrial and energy-related emissions before it can be transported, utilized, or permanently stored, making capture the essential first stage of every carbon capture and storage project. The segment continues to benefit from improved process efficiency, better plant integration, and enhanced operating reliability, encouraging wider deployment across large industrial facilities seeking to reduce emissions.

The transportation segment is steadily expanding as industries invest in shared pipelines, shipping networks, and integrated hub infrastructure. These systems connect capture facilities with utilization sites and permanent storage locations, supporting larger carbon management networks and improving project efficiency. As transport infrastructure develops, it is expected to become an increasingly important component of future carbon capture and storage projects.

Technology Analysis

Post-Combustion Capture accounted for more than 50.00% of the market in 2025. The technology remains widely adopted because it removes carbon dioxide after fuel combustion, allowing operators to retrofit existing industrial plants and power facilities without major modifications to their primary production processes. Its compatibility with sectors including power generation, cement, chemicals, and other emission-intensive industries has strengthened its market position. Continuous improvements in solvent systems, equipment design, energy efficiency, and process integration are also enhancing capture performance and operational reliability.

Pre-Combustion Capture is gaining momentum in hydrogen production, gasification projects, and integrated industrial developments where carbon dioxide can be removed before combustion. Its suitability for concentrated gas streams supports efficient carbon removal and strengthens its potential in future low-carbon industrial applications.

Capture Source Analysis

Point Source Capture (Industrial Stacks) dominated the market with more than 84.50% share in 2025. Industrial facilities generate concentrated carbon dioxide emissions through exhaust stacks, making these locations practical for installing capture systems, monitoring emissions, and connecting to transportation and storage infrastructure. The segment continues to benefit from widespread adoption across power generation, cement manufacturing, steel production, chemicals, refining, and other heavy industrial operations where emissions remain stable and measurable.

Growing interest is also emerging in Distributed / Mobile Source Capture, where industries are exploring carbon removal from smaller and mobile emission sources. Advancements in compact capture technologies, modular systems, and flexible collection methods are supporting the gradual development of this segment across transport fleets and dispersed industrial facilities.

End-Use Industry Analysis

The Oil & Gas industry maintained its leading position with more than 42.00% of the market in 2025. Existing infrastructure, including gas processing facilities, pipelines, underground reservoirs, and operational expertise, enables companies to integrate carbon capture, transportation, and permanent storage more efficiently. Industry experience in subsurface evaluation, well management, pressure control, and long-term monitoring further supports widespread CCS deployment.

The Power Generation sector is emerging as an important growth area as utilities pursue emission reduction strategies for existing thermal power plants. Carbon capture retrofit projects, combined with access to shared transport and storage infrastructure, are supporting increased adoption within the power sector.

Key Market Segments

By Service

- Capture

- Transportation

- Utilization

- Storage

By Technology

- Post-Combustion Capture

- Pre-Combustion Capture

- Oxy-Fuel Combustion Capture

- Others

By Capture Source

- Point Source Capture (Industrial Stacks)

- Distributed / Mobile Source Capture

- Direct Air Capture (Atmospheric)

By End-Use Industry

- Oil & Gas

- Power Generation

- Industrial (Cement, Fertilizers & Others)

- Others

Driving Factors

The market is primarily driven by expanding government policies and infrastructure supporting carbon capture and storage. The European Union has established a legally binding target of at least 50 million tonnes of annual CO₂ injection capacity by 2030, alongside reporting obligations and contribution requirements for oil and gas producers. The Industrial Carbon Management Strategy also projects 50 Mt of annual captured CO₂ by 2030, 280 Mt by 2040, and 450 Mt by 2050, while estimating approximately €3 billion for storage facilities and €6.2–9.2 billion for transport infrastructure. These initiatives encourage shared transport and storage hubs, reduce infrastructure risks, improve project economics, and support wider commercial deployment across industrial regions.

Restraining Factors

The primary challenge facing the market remains the high cost of carbon capture. Complete carbon capture and storage chain costs range from approximately US$20–150 per tonne, with a weighted average of around US$58 per tonne globally. Hard-to-abate industries such as steel, cement, and chemicals may experience capture costs between US$75–100 per tonne or higher after accounting for flue gas dilution, retrofit requirements, impurities, and energy consumption. Since nearly two-thirds of total project costs occur during the initial stages, developers continue to face significant capital expenditure and operational cost pressures, slowing investment decisions and limiting deployment primarily to projects supported by strong policy incentives.

Growth Opportunity

An emerging opportunity lies in producing advanced carbon materials from captured CO₂ through mineralization technologies. This market was valued at approximately US$820 million in 2025 and is projected to reach US$1.86 billion by 2034. Mineralization permanently converts captured carbon into construction aggregates, concrete, and carbonation-cured products, creating additional commercial value beyond geological storage. Partnerships between carbon capture operators, materials science companies, specialty chemical producers, and construction material manufacturers could transform captured carbon into valuable industrial feedstocks. A 1 Mtpa capture facility directing 10%–20% of captured CO₂ into mineralization products valued between US$200–500 per tonne could generate approximately US$20–100 million in annual incremental revenue, supporting future market expansion as material standards and construction codes continue to evolve.