Active Toughening Agent for Epoxy Resin Market Strategic Insights

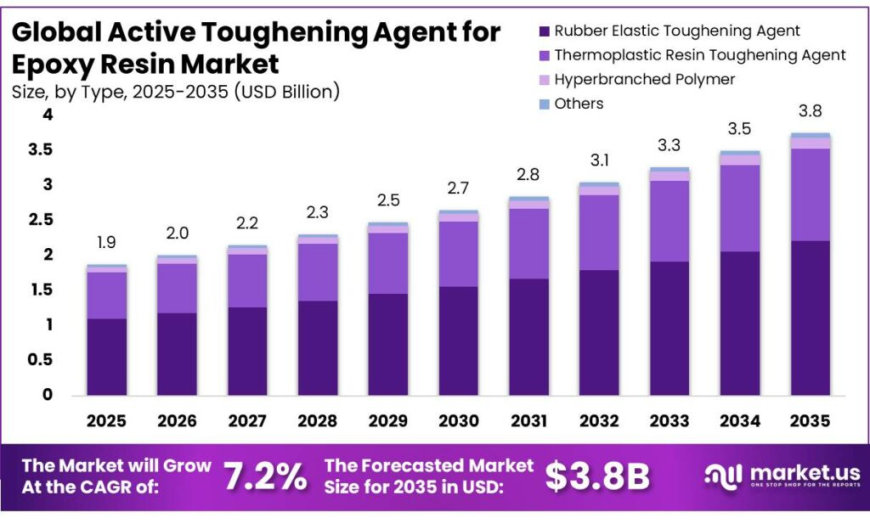

The Active Toughening Agent for Epoxy Resin Market is valued at USD 1.9 billion in 2025 and is projected to reach USD 3.8 billion by 2035, growing at a CAGR of 7.2%.https://market.us/report/active-toughening-agent-for-epoxy-resin-market/

sonicbolt20

sonicbolt20

## Overview

The **[Active Toughening Agent for Epoxy Resin Market](https://market.us/report/active-toughening-agent-for-epoxy-resin-market/)** stood at **USD 1.9 billion in 2025** and is forecast to reach **USD 3.8 billion by 2035**, at a **CAGR of 7.2% (2026–2035)**. Growth is strongly influenced by aerospace, automotive, and EV applications requiring high-performance epoxy systems. The **Electronics segment**, with **43.4% share**, dominates due to increasing semiconductor production valued at **US$630.5 billion in 2024**. Demand for advanced encapsulation materials continues to support market expansion globally.

## Key Takeaways

* Market size reached **USD 1.9 billion in 2025**.

* Forecast value expected to reach **USD 3.8 billion by 2035**.

* Market growth at **CAGR of 7.2% (2026–2035)**.

* **Asia Pacific** dominated with **55.0% share (USD 1.03 Billion)** in 2025.

* **Rubber Elastic Toughening Agent** led with **58.8% share**.

* **Electronics segment** held **43.4% share**.

* **Building & Construction** dominated end-use with **48.5% share**.

* Demand supported by epoxy reinforcement in high-stress environments and advanced composite systems.

## Analysis Sections

## Type Analysis

The **Rubber Elastic Toughening Agent** segment dominated the **Active Toughening Agent for Epoxy Resin Market**, accounting for **58.8% share in 2025**. These materials, including CTBN (carboxyl-terminated butadiene-acrylonitrile) and ATBN (amine-terminated butadiene-acrylonitrile), integrate into epoxy systems and phase-separate during curing to prevent micro-crack propagation. This improves toughness, durability, and resistance under mechanical stress.

According to the **International Rubber Study Group (IRSG)**, global synthetic rubber consumption reached **291 million metric tonnes in 2024**, rising **1.1%** from **16.107 million metric tonnes in 2023**. This expanding elastomer base supports increased availability of butadiene-based modifiers used in epoxy toughening systems for industrial-grade applications.

## Application Analysis

The **Electronics segment** accounted for **43.4% share in 2025**, driven by the need for reliable encapsulation and protection of semiconductor components against thermal and mechanical stress. Epoxy systems enhanced with active toughening agents are widely used in microelectronic packaging and underfill applications to prevent structural failure under fluctuating operational conditions.

According to the **World Semiconductor Trade Statistics (WSTS)**, global semiconductor sales reached approximately **US$630.5 billion in 2024**, supporting demand for advanced epoxy encapsulants and high-performance protective materials. Additionally, coating innovations such as self-healing epoxy systems are expanding use cases in offshore and marine environments, where crack resistance and moisture protection are critical.

## End-Use Analysis

The **Building & Construction segment** dominated with **48.5% share in 2025**, supported by extensive use in structural bonding, concrete repair, flooring systems, and anchoring applications. These environments require epoxy systems with high load-bearing capacity and long-term durability under harsh conditions.

According to the **U.S. Census Bureau**, construction spending reached approximately **US$2.20 trillion in February 2025**, increasing **9% from February 2024**, reinforcing demand for advanced epoxy-based materials. The **Marine segment** is emerging rapidly due to offshore wind and tidal turbine structures requiring high fatigue resistance and long-term structural stability under saltwater exposure.

## Key Market Segments

By Type, the market includes **Rubber Elastic Toughening Agent**, **Thermoplastic Resin Toughening Agent**, **Hyperbranched Polymer**, and **Others**.

By Application, it includes **Electronics**, **Coating**, **Adhesive**, and **Others**.

By End-use, it includes **Building & Construction**, **Automotive & Transportation**, **Electrical & Electronics**, **Marine**, and **Others**.

## Driving Factors

The **Active Toughening Agent for Epoxy Resin Market** is strongly driven by regulatory and industrial transformation pressures. The implementation of **EU Regulation (EU) 2024/3190**, effective from **20 January 2025**, along with phased compliance deadlines extending to **20 July 2026**, **20 July 2028**, **20 January 2028**, and **20 January 2029**, is accelerating reformulation of epoxy systems toward alternative modifier packages. Similarly, **California AB 1148**, effective from **1 January 2027**, is increasing demand for non-BPA epoxy systems.

These regulatory shifts are increasing R&D investment in reactive liquid rubbers, core-shell particles, and hyperbranched polymers, all of which enhance toughness while maintaining compliance. Additional demand is supported by aerospace lightweighting trends and EV power electronics requiring crack-resistant epoxy materials.

## Restraining Factors

The market faces significant constraints from regulatory delays and chemical approval bottlenecks. The **TSCA new-chemicals review process** in North America has created extended qualification timelines of **6–18 months**, significantly beyond the statutory **90-day window**. Each PMN cycle costs approximately **US$200,000–US$500,000**, increasing commercialization barriers for new toughening chemistries.

Additional restraints include volatility in natural rubber and elastomer feedstock prices, Superfund excise taxes on acrylonitrile-butadiene rubber in North America, and EU BPA-related compliance burdens that extend R&D timelines and increase formulation costs. Trade uncertainties and high energy costs further compress margins across global production systems.

## Growth Opportunity

A major growth opportunity lies in **formulation-as-a-service and licensing-based monetization models**. Instead of purely selling material volumes, manufacturers are increasingly shifting toward bundled solutions that include formulation optimization, curing process design, and technical support services. This approach reduces customer qualification time by **3–9 months** in regulated applications and enhances supplier profitability.

By transitioning to service-based revenue models, suppliers can achieve **4–8 percentage point EBITDA expansion**, as technical services generate higher margins compared to raw material sales. This evolution positions active toughening agents not only as material inputs but also as integrated solution platforms for advanced epoxy system performance optimization.

👉 Step 1 completed. Do you want Step 2: Alternative Overview?