Electric Vehicle Battery Market Size Analysis with Industry Forecast

The Commercial Battery Energy Storage As a Service Market was valued at USD 1.2 billion in 2025 and is projected to reach USD 6.9 billion by 2035, growing at a CAGR of 19.7%. https://market.us/report/electric-vehicle-battery-market/

sonicbolt20

sonicbolt20

Overview

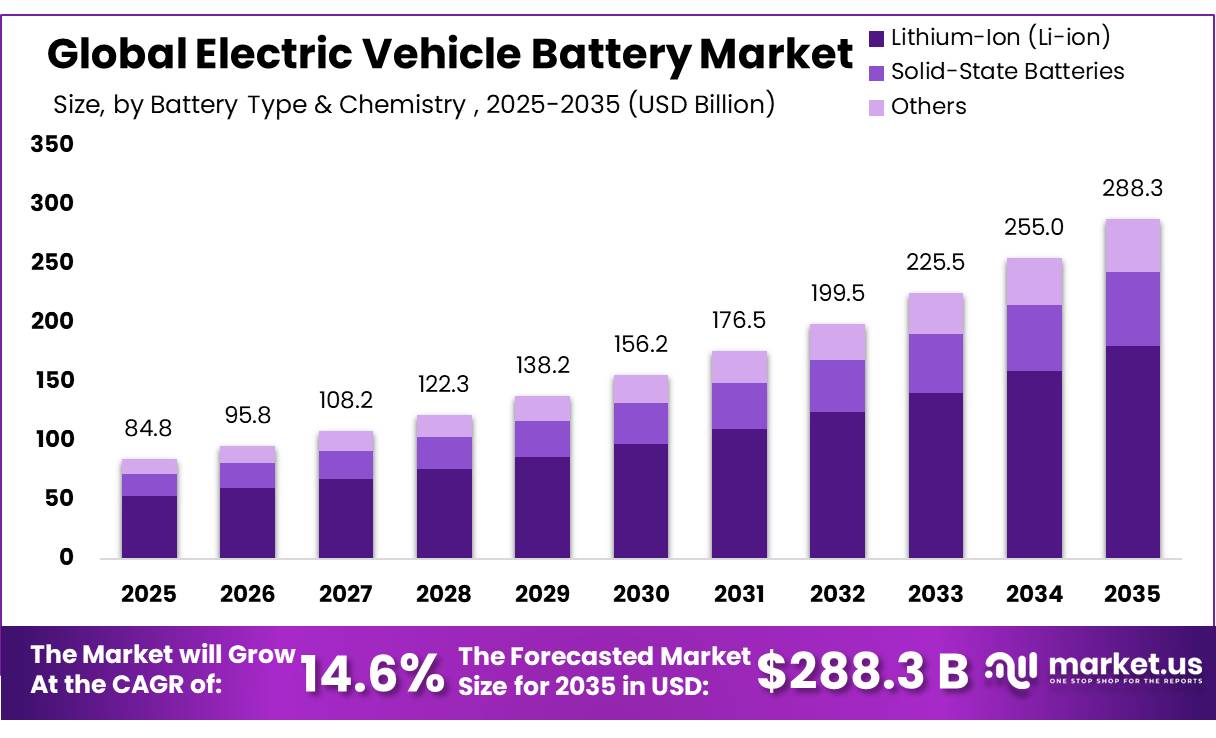

The Electric Vehicle Battery Market generated USD 84.8 billion in 2025 and is projected to reach USD 288.3 billion by 2035, advancing at a CAGR of 14.6%. North America captured a leading 35.6% market share with USD 30.19 billion in revenue. Growing demand for electric passenger vehicles, expanding battery production facilities, declining lithium-ion battery prices, and innovations in battery technologies are supporting long-term industry expansion.

Key Takeaways

- The Global Electric Vehicle Battery Market was valued at approximately USD 84.8 billion in 2025.

- The global Market is projected to grow at a CAGR of 14.6% and is estimated to reach nearly USD 288.3 billion by 2035.

- On the basis of battery type & chemistry, Lithium-Ion (Li-ion) batteries dominated the market, constituting 62.50% of the total market share.

- Based on vehicle type, Passenger Cars dominated the market, accounting for 62.50% of the total market share.

- Based on material type, Cobalt led the market with a 28.50% share, followed closely by Lithium at 27.3%.

- Among propulsion types, Battery Electric Vehicles (BEVs) dominated the market, accounting for 58.60% of the total market share.

- Based on battery capacity, the 15 kWh–50 kWh segment accounted for the largest market share at 50.20%, driven by strong adoption in mainstream passenger EVs.

- By battery form, Prismatic batteries dominated the market with a 44.5% share

- In 2025, North America emerged as the dominant regional market, accounting for 35.60% of the global Electric Vehicle Battery Market share.

Battery Type & Chemistry Analysis

Lithium-Ion (Li-ion) batteries dominated the market in 2025, accounting for more than 62.50% of total revenue. Their leadership is supported by high energy density, long operating life, rapid charging capability, and reliable performance across passenger cars, buses, commercial vehicles, and electric two-wheelers. Continuous improvements in battery management systems, thermal control, and cell chemistry have further strengthened their market position through June 2026.

Solid-State Batteries continue to emerge as a promising segment due to their potential to deliver greater safety, higher energy density, and longer driving range. Battery manufacturers and vehicle producers are expanding pilot production and testing activities to accelerate commercial deployment.

Vehicle Type Analysis

Passenger Cars represented the largest application segment, capturing more than 62.5% of the market in 2025. Rising electric passenger vehicle sales, broader model availability across compact cars, sedans, and SUVs, along with lower battery costs and expanding charging infrastructure, continue to support battery demand. Government initiatives promoting cleaner transportation also contribute to sustained market growth.

Commercial Vehicles are witnessing strong growth as fleet operators increasingly electrify delivery vans, buses, and trucks. Lower operating costs, stricter emission regulations, and demand for cleaner urban mobility are driving investments in larger and more durable battery systems.

Material Type Analysis

Cobalt held a dominant market position with more than 28.50% share during 2025. The material remains critical for improving battery stability, energy density, thermal performance, and operational life, particularly in premium and long-range electric vehicles. Battery manufacturers are simultaneously working to reduce cobalt intensity through advanced cathode designs while maintaining battery performance.

Lithium continues to emerge as a fast-growing material segment because it remains an essential component across most rechargeable electric vehicle battery chemistries. Rising battery production capacity, investments in recycling, and expansion of lithium-based technologies are strengthening long-term demand.

Propulsion Analysis

Battery Electric Vehicles (BEVs) dominated the market with a 58.60% share in 2025. Since BEVs rely entirely on battery power, they require larger battery packs than hybrid alternatives, creating higher battery demand per vehicle. Ongoing improvements in driving range, charging speed, battery durability, and thermal management continue supporting adoption.

Plug-in Hybrid Electric Vehicles (PHEVs) are also expanding as they combine electric propulsion with internal combustion engines, offering greater flexibility in markets where charging infrastructure remains under development.

Battery Capacity Analysis

The 15 kWh–50 kWh battery capacity segment accounted for more than 50.20% of the market in 2025. This capacity range remains widely adopted in compact electric vehicles, city cars, plug-in hybrids, and affordable passenger models because it offers an effective balance between driving range, battery cost, charging time, and vehicle weight.

The 50 kWh–110 kWh segment is expanding steadily as consumers increasingly demand longer driving ranges and improved vehicle performance across premium passenger vehicles, SUVs, and commercial fleets.

Battery Form Analysis

Prismatic batteries led the market with a 44.50% share during 2025. Their rectangular design enables efficient battery pack integration, improved structural stability, higher energy storage, and simplified assembly processes. These advantages make prismatic cells suitable for passenger vehicles, buses, and commercial transportation.

Cylindrical batteries continue gaining attention because of their mature manufacturing process, reliable thermal performance, and mechanical durability, particularly in high-performance electric vehicles.

Key Market Segments

By Battery Type & Chemistry

- Lithium-Ion (Li-ion)

- LFP (Lithium Iron Phosphate)

- NMC (Nickel Manganese Cobalt)

- NCA (Nickel Cobalt Aluminum)

- Solid-State Batteries

- Others

By Vehicle Type

- Passenger Cars

- Sedans

- SUVs / Crossovers

- Hatchbacks

- Commercial Vehicles

- Light Commercial Vehicles (LCV) / Vans

- Medium & Heavy Trucks

- Buses & Coaches

- Two-Wheelers & Three-Wheelers

- Others

By Material Type

- Cobalt

- Lithium

- Natural Graphite

- Manganese

- Others

By Propulsion

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid Electric Vehicle (PHEV)

- Hybrid Electric Vehicle (HEV)

By Battery Capacity

- <15 kWh

- 15 kWh–50 kWh

- 50 kWh–110 kWh

- >110 kWh

By Battery Form

- Cylindrical

- Prismatic

- Pouch

Driving Factors

Declining battery costs remain one of the strongest growth drivers for the Electric Vehicle Battery Market. Lithium-ion battery pack prices have declined by 89% since 2010, falling from over USD 1,000/kWh to USD 108/kWh in 2025. Forecasts indicating prices near USD 80/kWh by 2026 are expected to bring battery electric vehicles closer to total ownership cost parity with gasoline-powered vehicles. At the same time, expanding Gigafactory investments, government ZEV mandates, increasing EV sales volumes, advances in cell architecture, and commercialization of Solid-State Batteries continue strengthening market demand globally.

Restraining Factors

The market continues to face significant challenges from the concentration of critical mineral supply chains. China controls 70–80% of global lithium and cobalt refining capacity, around 30% of nickel processing, nearly 90% of rare earth element separation, and approximately 79% of global natural graphite production. This concentration exposes manufacturers in North America, the European Union, and India to higher raw material costs, supply chain disruptions, and increased dependence on imported battery materials. High capital requirements, charging infrastructure limitations, evolving safety regulations, and skilled workforce shortages further restrain market growth.

Growth Opportunity

Battery-as-a-Service (BaaS) and battery swapping models present significant growth opportunities for the Electric Vehicle Battery Market, particularly across India, Indonesia, and Vietnam. In India, where two- and three-wheelers account for more than 57% of EV registrations, BaaS penetration remains below 3% of the addressable market exceeding 10 million units annually. This creates a potential subscription revenue opportunity of USD 8–12 billion per year at USD 15–20 per vehicle per month. By retaining battery ownership, operators can benefit from second-life battery value, optimized charging cycles, and electricity procurement costs that are 20–35% below retail rates, supporting gross margins of 30–45% compared with 8–15% for conventional battery hardware businesses.