Chlorine Market Strategic Outlook for Global Industry

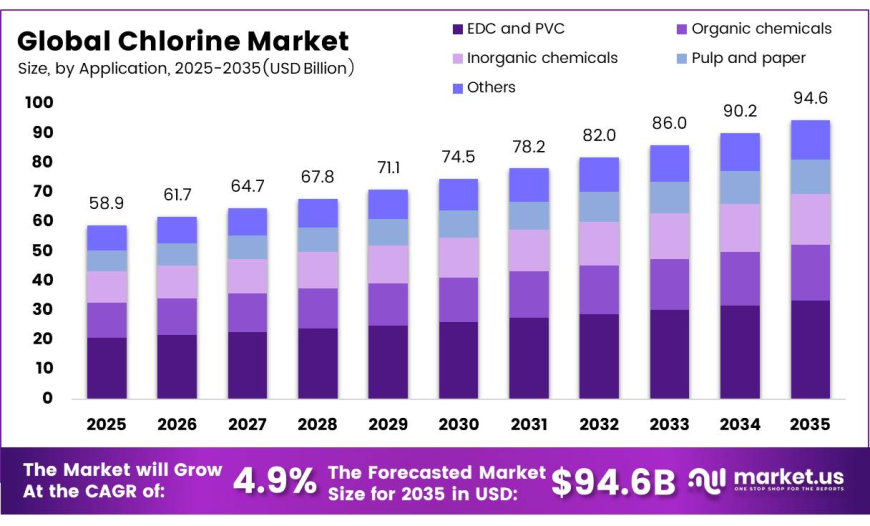

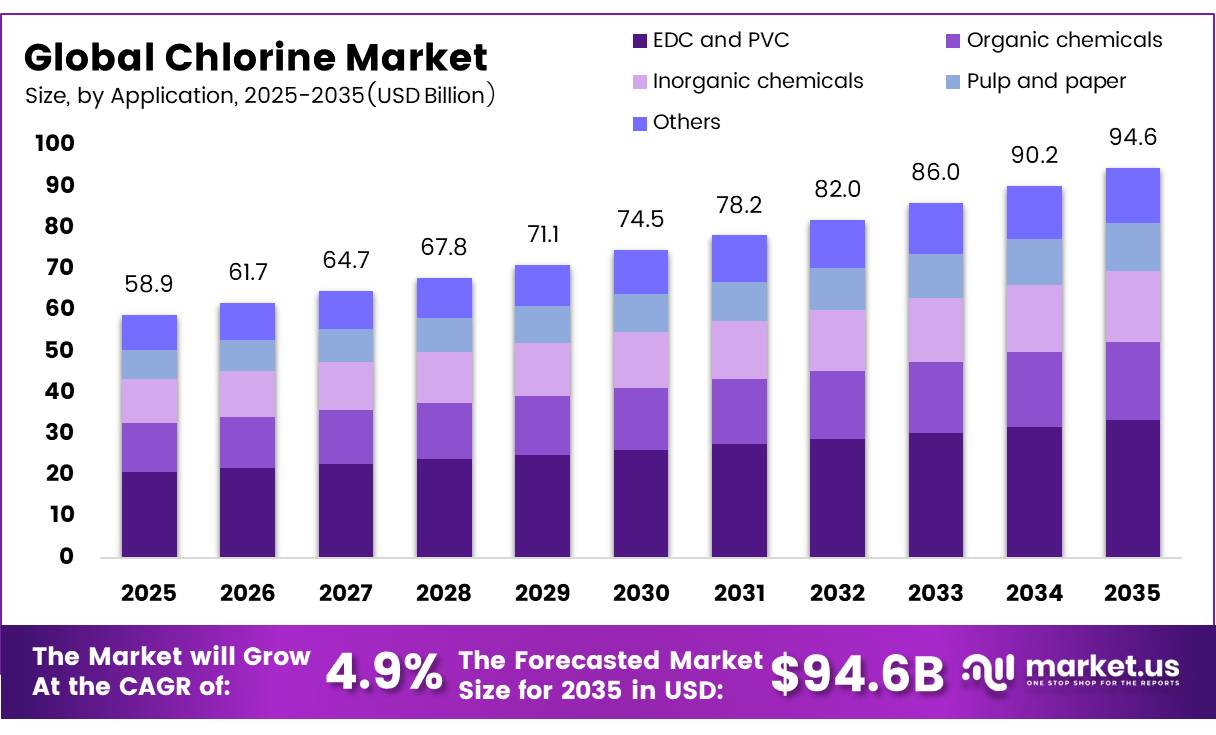

Explore the Chlorine Market analysis covering market size of USD 58.9 billion in 2025, projected to reach USD 94.6 billion by 2035 at a 4.9% CAGR. https://market.us/report/chlorine-market/

sonicbolt20

sonicbolt20

Overview

Chlorine Market accounted for USD 58.9 billion in 2025 and is projected to rise to USD 94.6 billion by 2035, recording a CAGR of 4.9%. Asia Pacific maintained its leading position with 40.7% of the global market and revenue of USD 23.9 billion in 2025. Chlorine remains a fundamental raw material across the chlor-alkali industry, supporting applications in PVC, water treatment, paper processing, chemical production, and pharmaceutical manufacturing. Increasing investments in industrial and municipal infrastructure continue to support market expansion.

Key Takeaways

- The Global Chlorine Market was valued at USD 58.9 billion in 2025.

- The market is projected to reach USD 94.6 billion by 2035, growing at a CAGR of 4.9%.

- By Form, Liquid Chlorine dominated the market with a 65.1% share.

- By Application, EDC and PVC accounted for the largest share of 35.2%.

- By End User, the Chemicals segment led the market with a 39.9% share.

- Asia Pacific remained the leading regional market, accounting for 40.7% of the global market in 2025.

Form Analysis

In 2025, Liquid Chlorine held the leading market position, accounting for more than 65.1% of the market. Its dominance was supported by extensive use across water treatment, chemical manufacturing, pulp and paper processing, and disinfectant production. The ability to store and transport liquid chlorine efficiently in pressurized containers makes it highly suitable for large municipal facilities and industrial operations. By June 2026, demand remained stable as industries continued to depend on liquid chlorine for accurate dosing, dependable supply, and seamless integration into existing production systems.

Gaseous Chlorine continues to emerge as a growing segment due to its strong oxidation capability and rapid disinfection performance. It is primarily used in facilities equipped with dedicated handling, monitoring, and safety systems, particularly in large-scale water treatment and chemical processing operations where controlled gas applications are required.

Application Analysis

In 2025, EDC and PVC represented the largest application segment, capturing more than 35.2% of the market. The segment maintained its leadership because chlorine is an essential raw material for producing ethylene dichloride (EDC), which serves as the primary feedstock for manufacturing vinyl chloride and PVC. Continuous demand from pipes, flooring, window profiles, cables, medical products, and packaging sustained chlorine consumption across this application.

The Organic Chemicals segment is also witnessing steady growth as chlorine remains an important processing agent and intermediate in the production of solvents, refrigerants, pharmaceuticals, agrochemicals, and specialty chemicals. The expanding diversity of manufacturing industries continues to support consistent demand within this application category.

End User Analysis

In 2025, the Chemicals segment accounted for more than 39.9% of the global market, making it the leading end-user industry. Chlorine remains a critical raw material for manufacturing solvents, intermediates, bleaching agents, disinfectants, and numerous industrial chemical products. Large integrated chlor-alkali facilities require a continuous chlorine supply to maintain efficient production, reinforcing the segment's dominant position.

The Plastics segment continues to gain importance as chlorine remains indispensable in PVC production. Growing demand for construction materials, pipes, cables, packaging, medical products, and durable plastic components continues to support chlorine consumption across this end-user category.

Key Market Segments

By Form

- Liquid Chlorine

- Gaseous Chlorine

By Application

- EDC and PVC

- Organic Chemicals

- Inorganic Chemicals

- Pulp and Paper

- Others

By End User

- Chemicals

- Plastics

- Water Treatment

- Paper and Pulp

- Pharmaceuticals

- Pesticides and Other Industries

Driving Factors

Investment in Water Treatment Infrastructure remains one of the strongest long-term growth drivers for the market. Around 2.2 billion people worldwide still lack access to safe drinking water, while only 74% of the global population had access to safely managed drinking water in 2024, compared with 68% in 2015. Achieving global SDG 6 objectives requires approximately USD 114 billion in annual WASH investment, creating sustained demand for chlorine-based water disinfection systems.

In the United States, municipal drinking water and wastewater applications consumed approximately 628 million kg of chlorine annually, representing nearly 5% of total domestic chlorine production. As governments continue upgrading aging water infrastructure, chlorine demand is expected to become increasingly supported by long-term municipal investments. Chlorination also remains the most economical and scalable disinfection technology because it combines broad-spectrum effectiveness, residual protection throughout distribution systems, and low operating costs. Growing adoption of electrochloration systems, which represented 36.5% of the injection product mix by 2026, is further reshaping chlorine production and distribution economics.

Restraining Factors

The market continues to face significant pressure from the Extreme Energy Cost Burden on Chlor-Alkali Production, particularly across Europe. Chlor-alkali manufacturing is highly electricity intensive, and elevated industrial electricity prices continue to reduce profitability for producers. While electricity prices previously averaged EUR 40–60 per MWh, they increased to EUR 150–250 per MWh during 2022–2023 and remained at EUR 80–130 per MWh throughout 2025–2026. At approximately EUR 100 per MWh, electricity costs alone account for EUR 250–300 per tonne of chlorine produced through membrane-cell technology.

Although policy measures such as the European Commission's Clean Industrial Deal and Germany's EUR 0.05 per kWh industrial electricity subsidy aim to provide support, many facilities continue operating below economically sustainable utilization levels. Lower-cost production regions such as Asia Pacific and the Middle East, where industrial electricity prices range between USD 0.04–0.07 per kWh, continue attracting new chlor-alkali investments, contributing to a structural shift in global production capacity.

Growth Opportunity

A significant growth opportunity lies in Green Chlorine Co-Production Monetization. A large chlor-alkali facility producing 200,000 tonnes of chlorine annually also generates approximately 5,600 tonnes of hydrogen. With certified hydrogen prices ranging from USD 3–5/kg, producers can potentially create an additional USD 11–22 million in annual revenue from hydrogen sales alone.

Producers can also reduce electricity costs by up to 22% and lower CO₂ emissions by up to 10% by 2040 through load-shifting electrolysis operations to periods of surplus renewable energy. The launch of INEOS Inovyn's Ultra Low Carbon Chlor-Alkali range in 2024, which achieved a 70% reduction in CO₂ emissions, demonstrates the commercial potential of low-carbon chlorine production. Companies investing in hydrogen purification, certified green hydrogen production, and long-term off-take agreements could benefit from an estimated 2.2 percentage point increase in CAGR between 2028 and 2033, creating substantial long-term growth potential.